영어/한국어 웹사이트

한국어? 위에서 선택

Looking for a home mortgage loan from a reliable lender?

NY / NJ / FL / GA

(718)844-8608Get a Home Mortgage Loan

Lower, Simpler, Faster, Easier, and Safer!

Programs that waive income and tax documentation

What we do

Some useful information

Down payment amount, income, and especially FICO score! These are the key determinants!

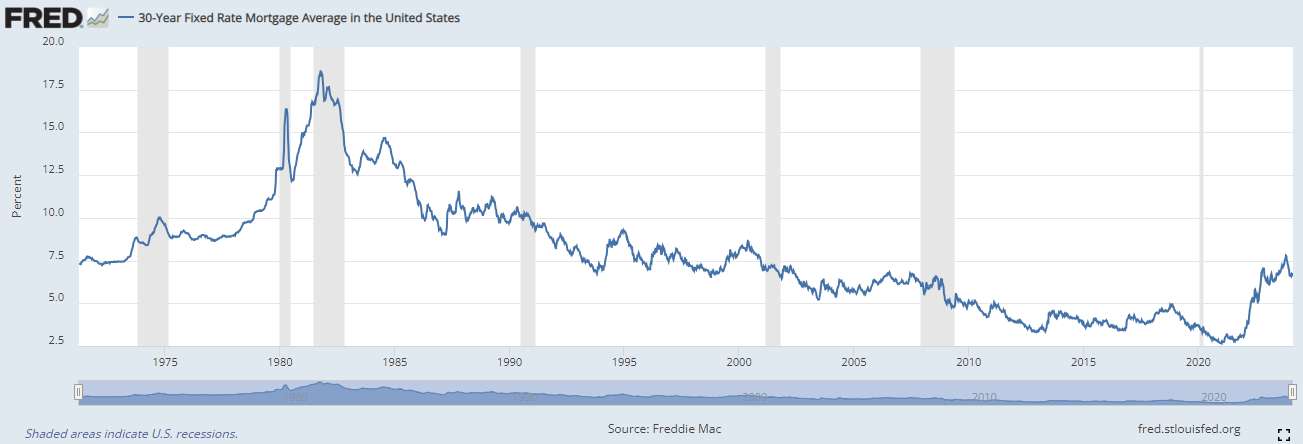

Mortgage interest rate trends over the past 30 years

15k+ clients worldwide use our products

About Mortgage Loans

Have SomeThat You Want to Share

FAQ

일반적으로 집을 찾아 계약하고 클로징까지 대략 두 달 안팎이 걸립니다. 여러 가지 해야 할 일이 있기 때문이죠.

대부분의 일은 집이 법적으로 안전한가를 확인합니다. 그리고 구매자가 인스펙션을 하면서 집 주인과 딜도 해야 하구요. 그리고 론 컴퍼니는 집 감정을 해야 합니다. 이런 여러 가지 일들이 진행되면서 시간이 좀 걸리는 것이죠.

Our streamlined process delivers a pre-approval letter within just 20 minutes of a brief phone interview. Once all documents are submitted, we can close your loan in as little as 10 days.

그리고 정말 바쁘다면 10일, 일반적인 경우에 한 달이면 충분히 모든 준비가 마쳐질 수 있습니다.

You can rely on us to help you secure the perfect home.

대부분의 일은 집이 법적으로 안전한가를 확인합니다. 그리고 구매자가 인스펙션을 하면서 집 주인과 딜도 해야 하구요. 그리고 론 컴퍼니는 집 감정을 해야 합니다. 이런 여러 가지 일들이 진행되면서 시간이 좀 걸리는 것이죠.

Our streamlined process delivers a pre-approval letter within just 20 minutes of a brief phone interview. Once all documents are submitted, we can close your loan in as little as 10 days.

그리고 정말 바쁘다면 10일, 일반적인 경우에 한 달이면 충분히 모든 준비가 마쳐질 수 있습니다.

You can rely on us to help you secure the perfect home.

Various factors determine your interest rate, with the primary ones being your FICO score, down payment amount, and loan amount.

Essentially, we review your credit report, which reflects your financial history and creditworthiness. Once your credit profile is approved, we can provide you with suitable loan options.

A FICO score of 720 or higher is recommended. Below may result in higher rates.

A down payment of 30% or more is ideal. Lower amounts may increase your rate.

A loan amount of $300,000 or more is ideal. Smaller loan amounts may carry higher rates.

If rates drop even further as these figures improve? Unfortunately, that isn’t the case. These factors are the minimum requirements to avoid higher rates.

Please note that interest rates may be higher for second homes, condos, or investment properties.

Essentially, we review your credit report, which reflects your financial history and creditworthiness. Once your credit profile is approved, we can provide you with suitable loan options.

A FICO score of 720 or higher is recommended. Below may result in higher rates.

A down payment of 30% or more is ideal. Lower amounts may increase your rate.

A loan amount of $300,000 or more is ideal. Smaller loan amounts may carry higher rates.

If rates drop even further as these figures improve? Unfortunately, that isn’t the case. These factors are the minimum requirements to avoid higher rates.

Please note that interest rates may be higher for second homes, condos, or investment properties.

Nothing happens!

In the past, borrowers who paid off their loans earlier than the scheduled term faced prepayment penalties. However, these penalties have been eliminated in most loan programs today.

단 일을 처리하면서 발생한 모든 수수료에 대한 문제가 발생합니다. 그래서 통상 1년 정도 내에서는 리파이넌스나 판매를 하지 않는 것이 일반적입니다.

그리고 pay off를 하거나 Refinance를 할 때는 당연히 나머지 원금은 모두 갚아야 합니다. 그래서 미리 손을 터는 것이 좋은가 아닌가는 약간 생각해 볼 가치가 있는데….

First of all, the loan is typically set for 30 years, with payments calculated equally over that period. However, during the early stages of the loan, you pay less toward the principal and more toward the interest. In other words, if you pay off the loan early on, you might find that you've mostly just paid interest while the principal remains largely untouched.

It's always a good thing to be debt-free, so if you have the money, it's probably best to just pay it off.

In the past, borrowers who paid off their loans earlier than the scheduled term faced prepayment penalties. However, these penalties have been eliminated in most loan programs today.

단 일을 처리하면서 발생한 모든 수수료에 대한 문제가 발생합니다. 그래서 통상 1년 정도 내에서는 리파이넌스나 판매를 하지 않는 것이 일반적입니다.

그리고 pay off를 하거나 Refinance를 할 때는 당연히 나머지 원금은 모두 갚아야 합니다. 그래서 미리 손을 터는 것이 좋은가 아닌가는 약간 생각해 볼 가치가 있는데….

First of all, the loan is typically set for 30 years, with payments calculated equally over that period. However, during the early stages of the loan, you pay less toward the principal and more toward the interest. In other words, if you pay off the loan early on, you might find that you've mostly just paid interest while the principal remains largely untouched.

It's always a good thing to be debt-free, so if you have the money, it's probably best to just pay it off.

이 문제는 주에 따라 다르게 적용됩니다.

우리는 처음 론을 시작할 때 확인해서 적용 가능하다면 자동으로 적용시켜 처리해 드립니다.

우리는 처음 론을 시작할 때 확인해서 적용 가능하다면 자동으로 적용시켜 처리해 드립니다.

FHA loans are well-known for requiring a smaller down payment and providing various benefits.

일반적으로 다운페이를 3.5% 까지만 해도 되는 것으로 알려졌는데 그건 사실입니다. 그리고 일반적으로 다운페이 금액이 적으면 이자율이 올라가는데 FHA에서는 다운페이 금액이 이자율에 직접 연동되지는 않습니다. 이건 장점으로 보입니다.

하지만 다운페이가 얼마든 론이 지속되는 평생 론 금액의 1% 안팎의 보험금을 매달 내야하며 처음 신청시 무조건 1.7%를 추가로 내야 합니다.

단 장점도 있습니다. DTI 그러니까 보다 적은 인컴으로 좀 더 높게 론을 받을 수 있습니다. 그리고 FICO score가 580 이상이면 됩니다. 이건 매우 큰 장점이죠.

간단하게 정리하면 이렇습니다. 최근에 FICO score가 푹 떨어졌다. 학자금 자동차 등등 매달 지출이 높다. 그러면 이 FHA가 이익일 수 있습니다. 하지만 일반적인 상황에서는 그냥 일반적인 론이 더 좋습니다.

일반적으로 다운페이를 3.5% 까지만 해도 되는 것으로 알려졌는데 그건 사실입니다. 그리고 일반적으로 다운페이 금액이 적으면 이자율이 올라가는데 FHA에서는 다운페이 금액이 이자율에 직접 연동되지는 않습니다. 이건 장점으로 보입니다.

하지만 다운페이가 얼마든 론이 지속되는 평생 론 금액의 1% 안팎의 보험금을 매달 내야하며 처음 신청시 무조건 1.7%를 추가로 내야 합니다.

단 장점도 있습니다. DTI 그러니까 보다 적은 인컴으로 좀 더 높게 론을 받을 수 있습니다. 그리고 FICO score가 580 이상이면 됩니다. 이건 매우 큰 장점이죠.

간단하게 정리하면 이렇습니다. 최근에 FICO score가 푹 떨어졌다. 학자금 자동차 등등 매달 지출이 높다. 그러면 이 FHA가 이익일 수 있습니다. 하지만 일반적인 상황에서는 그냥 일반적인 론이 더 좋습니다.

Full Documentation Loan vs. Low or No Documentation Loan. What documentation is required? It depends on how you prove your income—specifically, whether you provide tax-related documents (Full Doc) or not (No Doc).

Full doc is Qualified Mortgage Loans (QM), No doc is Non Qualified Mortgage Loans (Non QM).

차이는 No doc(nonQM) 이 약 0.5% 가량 이자율이 높습니다.

The primary difference between the two is that NonQM loans generally come with interest rates that are about 1% higher than those of QM loans. For income verification in Non-QM loans, 12 or 24 months of bank statements, VOE (Verification of Employment), and a P&L (Profit & Loss) letter can be used.

Full doc is Qualified Mortgage Loans (QM), No doc is Non Qualified Mortgage Loans (Non QM).

차이는 No doc(nonQM) 이 약 0.5% 가량 이자율이 높습니다.

The primary difference between the two is that NonQM loans generally come with interest rates that are about 1% higher than those of QM loans. For income verification in Non-QM loans, 12 or 24 months of bank statements, VOE (Verification of Employment), and a P&L (Profit & Loss) letter can be used.

When taking out a mortgage loan, it’s always a good idea to consider the possibility of refinancing in the future.

Refinancing involves replacing your current mortgage with a new one. If interest rates decrease, refinancing allows you to lower your mortgage interest rate. The process is typically straightforward and doesn’t require a significant amount of time or money. Most of our clients who take out loans with us are offered refinancing free of charge.

There are three main types of refinancing:

Rate-and-term refinance: This option focuses on reducing your interest rate and/or adjusting the loan term to better suit your financial goals. Cash-out refinance: With this option, you can borrow additional funds against your home’s equity while refinancing your mortgage.

The cash-out refinance is often referred to as borrowing money using your home as collateral. It enables homeowners to access the equity they’ve accumulated in their property. It it called HELOAN.

Refinancing involves replacing your current mortgage with a new one. If interest rates decrease, refinancing allows you to lower your mortgage interest rate. The process is typically straightforward and doesn’t require a significant amount of time or money. Most of our clients who take out loans with us are offered refinancing free of charge.

There are three main types of refinancing:

Rate-and-term refinance: This option focuses on reducing your interest rate and/or adjusting the loan term to better suit your financial goals. Cash-out refinance: With this option, you can borrow additional funds against your home’s equity while refinancing your mortgage.

The cash-out refinance is often referred to as borrowing money using your home as collateral. It enables homeowners to access the equity they’ve accumulated in their property. It it called HELOAN.

The mortgage interest rate quoted during your initial conversation with a Mortgage Loan Officer (MLO) is not guaranteed to stay the same. Interest rates fluctuate daily based on market conditions.

The process of securing the current rate at a specific point in time is referred to as “locking in” or a “rate lock.” Typically, it’s advisable to lock in your rate 15 to 30 days before closing. Until then, monitoring market conditions is recommended.

In some instances, your lender might unexpectedly increase the interest rate at the time of locking in. If this happens, please don’t hesitate to reach out to me for assistance.

The process of securing the current rate at a specific point in time is referred to as “locking in” or a “rate lock.” Typically, it’s advisable to lock in your rate 15 to 30 days before closing. Until then, monitoring market conditions is recommended.

In some instances, your lender might unexpectedly increase the interest rate at the time of locking in. If this happens, please don’t hesitate to reach out to me for assistance.

Banks typically display the Annual Percentage Rate (APR) alongside interest rates. The APR reflects the cost of loan-related fees expressed as a percentage of the loan amount, in addition to the interest rate. The difference between the APR and the interest rate is often around 0.06% of the loan amount, though this can vary depending on the loan terms and associated fees.

대략 론 금액의 0.2%가 정도가 됩니다.

대략 론 금액의 0.2%가 정도가 됩니다.

Obtaining a loan is generally a straightforward process.

You simply need to verify your income and show that your bank account has sufficient funds.

The remaining documents are relatively easy to handle, with no complicated calculations or analyses involved.

You simply need to verify your income and show that your bank account has sufficient funds.

The remaining documents are relatively easy to handle, with no complicated calculations or analyses involved.

When the price of crude oil rises, the gasoline prices we pay every day increase almost immediately.

However, in the reverse situation, gasoline prices tend to decrease much more slowly. This behavior is similar to how adjustable rates function.

고정과 변동은 상황에 따라 잘 결정하시는 것이 좋습니다.

However, in the reverse situation, gasoline prices tend to decrease much more slowly. This behavior is similar to how adjustable rates function.

고정과 변동은 상황에 따라 잘 결정하시는 것이 좋습니다.

Home Mortgage Loan for purchasing a home

Refinance to reduce current mortgage interest rates

Cash Out Refinance for lowering interest rates while freeing up some additional funds

HELOAN to secure funds using your home as collateral

Refinance to reduce current mortgage interest rates

Cash Out Refinance for lowering interest rates while freeing up some additional funds

HELOAN to secure funds using your home as collateral

If you’re ready to buy a house and have the financial means, but can’t prove your income through your tax returns, there are still options available to you.

This situation is often addressed with Non-Qualified Mortgages (Non-QM) or No Documentation (No Doc) loans.

현재 우리가 취급하는 no doc 은 크게 네 가지가 있습니다.

Alternative income documentation for Non-QM loans:

P&L letter addressed by a CPA

12 or 24 months of bank statements

1099 – 현재까지 받은 1099 form을 소득으로 인정하는 방법입니다.

Verification of Employment signed by the employer or HR.

DSCR, expected rental income from the home you are purchasing

This situation is often addressed with Non-Qualified Mortgages (Non-QM) or No Documentation (No Doc) loans.

현재 우리가 취급하는 no doc 은 크게 네 가지가 있습니다.

Alternative income documentation for Non-QM loans:

P&L letter addressed by a CPA

12 or 24 months of bank statements

1099 – 현재까지 받은 1099 form을 소득으로 인정하는 방법입니다.

Verification of Employment signed by the employer or HR.

DSCR, expected rental income from the home you are purchasing

If you're already living in the US and wish to stay, you can purchase a home even without permanent residency or citizenship.

A minimum of two years of residency in the US.

Stable and predictable income.

Strong credit profile.

Sufficient credit lines or existing equity.

최소 40% 이상 다운페이할 것

Evidence of financial stability for the next five years.

미국에 앞으로 장기간 살 것을 입증할 것. 물론 이런 것 모두 필요 없이 그냥 살 수도 있습니다.

A minimum of two years of residency in the US.

Stable and predictable income.

Strong credit profile.

Sufficient credit lines or existing equity.

최소 40% 이상 다운페이할 것

Evidence of financial stability for the next five years.

미국에 앞으로 장기간 살 것을 입증할 것. 물론 이런 것 모두 필요 없이 그냥 살 수도 있습니다.

HELOC 이란 Home Equity Line of Credit 입니다.

Line of Credit에서 보는 것처럼 마이너스 통장을 의미합니다. 즉 내가 필요한 돈의 액수를 정해 놓고 그 안에서 내가 필요한 만큼 쓰고 쓴 돈에 대해서만 이자를 갚는다는 것이죠. 즉 실제 돈을 받지 않았다면 낼 돈도 없다는 뜻입니다.

단 렌더들에게 이 상품은 살짝 위험 부담이 있습니다. 그래서 이자율이 높습니다.

하지만 안쓰면 내는 것도 없으니까 유사시에는 매우 효과적인 방법일 수 있습니다/

Line of Credit에서 보는 것처럼 마이너스 통장을 의미합니다. 즉 내가 필요한 돈의 액수를 정해 놓고 그 안에서 내가 필요한 만큼 쓰고 쓴 돈에 대해서만 이자를 갚는다는 것이죠. 즉 실제 돈을 받지 않았다면 낼 돈도 없다는 뜻입니다.

단 렌더들에게 이 상품은 살짝 위험 부담이 있습니다. 그래서 이자율이 높습니다.

하지만 안쓰면 내는 것도 없으니까 유사시에는 매우 효과적인 방법일 수 있습니다/

Balance (Gyunhyeong) Kim

T.(718)844-8608

General Mortgage Capital Corporation

NMLS #254895

1350 Bayshore Hwy, Suite 740, Burlingame, CA 94010

T.(650)340-7800